Following CREA failure, most large financial cooperatives begin 2026 with strong balance sheets

The failure of Cuenca-based CREA in July 2025 served as a wake-up call for Ecuador’s largest financial cooperatives, banking experts say. “It was a reminder that the traditional rules of good financial management still apply and that strong balance sheets are essential” says retired bank president Esteban Miller. “It appears that the lessons of the CREA collapse have been taken to heart by most of the coops.”

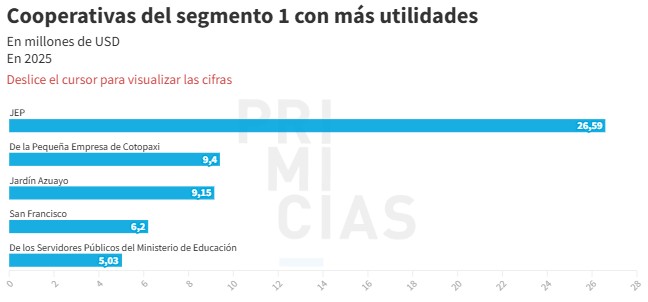

Cuenca-based JEP is the country’s largest financial cooperative.

According to the Superintendence of Popular and Solidarity Economy (SEPS), 42 of the country’s 43 largest cooperatives turned profits in 2025. Seps reports profits totaled $85.9 million compared to $29.3 million in 2024. Among the larger coops, only the National Police Cooperative ended the year in the red.

Another sign of the system’s financial health, SEPS reports, is that as of the end of January the solvency indicator for larger cooperatives was 18.3%, double the minimum of 9% required by law.

The cooperatives are an essential part of the national financial system because they serve segments of the population that banks do not, according to Miller. “They offer loans to people who have no credit history, or who have had credit problems in the past,” he says. “Because of this, they expect a higher rate of repayment delinquency than the banks. This is why they charge higher interest rates to borrowers. It is also why they pay higher returns on CDs and savings accounts.”

[Article continues below graphic)

The five financial cooperatives with the largest amount of assets. (Primicias)

In 2025, the average delinquency rate for cooperatives was 8.05% while it was 3% for banks.

Segundo Camino, economics professor at the Institute of Higher National Studies, agrees that the health of cooperatives is strong but points out they are exposed to a higher level of systemic risk than banks. “If there are sudden negative shocks to the economy, this can translate quickly to the bottom line,” he says. “Because of the exposure of higher risk loans, cooperative managers must perform a continuing balancing act to keep their institutions in good standing.”

Like Miller, Camino says the CREA failure was a “cautionary sale” for the system. “One of the outcomes is that SEPS is being more diligent in tracking cooperative data and making sure all reports are filed on time,” he says. “They have also increased the number of unscheduled audits of cooperatives.”

Camino adds that investors should understand the risk of putting money into cooperatives. “In the case of CREA and other failures, it was evident that many account holders were under the idea that cooperatives were the same as banks and this is not the case,” he said. “Yes, you are earning a much higher rate of return but there is a reason for this and this should be considered before investments are made. It is also important that investors know that their accounts are only insured by the government up to $32,000.”

He adds that cooperative members should consult the SEPS website for information about the financial status of their cooperative. “If you have trouble understanding the reports, have someone who does explain it to you,” he says.

In January 2026, SEPS reports the loan portfolio for the 43 largest cooperatives totals USD $15.635 billion while deposits totaled $20.4 billion.